📌 NEXA Lending + HCP COBRAND — CANONICAL LOGO (HECM lane)

Single source of truth for the NEXA Lending + Homestead Capital Partners cobrand lockup on Reverse Mortgage / HECM creative. Different compliance lane from DSCR (longer disclaimer band).

jhoward ir.attachment id=16767 · /web/image/16767 · logo_hcp_nexa_white.png

NEXA Lending — Reverse Mortgage (HECM) Creative

HECM Standard · HECM for Purchase · Equity Access · Retirement Income

Calm/dignified senior audience. FULL FHA + HECM compliance lane. Updated 2026-04-29.

📋 Product Categorization & Brand Mapping

Locked 2026-04-28. Source: reference_brand_to_product_mapping_2026-04-28.md in memory.

🏡 NEXA Lending HECM — Reverse Mortgage (this page only)

| Product | Description | Audience |

|---|---|---|

| HECM Standard | Home Equity Conversion Mortgage — line of credit / monthly draw / lump sum | 62+ existing homeowner |

| HECM for Purchase (H4P) | Buy a new primary residence with HECM at the same time | 62+ relocating / right-sizing |

| Equity Access | Use built-up equity without monthly mortgage payments | 62+ asset-rich / cash-light retiree |

| Retirement Income Strategy | Coordinate HECM with portfolio sequencing — fiduciary referral lane | 62+ planning-with-advisor |

🚨 Anti-patterns enforced on this page

- ❌ NO urgency / scarcity language (senior audience — calm / dignified only)

- ❌ NO "free money" / "government program" framing — HECM is a loan, not a benefit

- ❌ NO "lose your home" fear messaging — FTC §5 deceptive risk

- ❌ NO unverified senior-investment promises (Reg Z, MAP Rule)

- ❌ NO mixing DSCR / business funding / consumer mortgage messaging

- ❌ NO AXIA branding

- ❌ Caption MUST include: 62+ requirement, HUD counseling, not government benefit, repayment triggers

🔗 URL routing

- NEXA Reverse Mortgage:

/social/reverse-mortgage← this page (loans subdomain, HECM compliance lane) - NEXA DSCR:

/social/dscr-investoron dscr subdomain (mortgage compliance lane) - AXIA Capital:

/social/axia-capitalon business subdomain (non-mortgage)

⚖️ HECM Compliance Overlay — REQUIRED ON EVERY CREATIVE

Reverse Mortgage is FHA-insured + HUD-regulated. FTC §5 + 24 CFR 206 + Reg Z trigger-term rules apply on every ad. Caption MUST include the HECM disclaimer block — visible without "see more".

📋 Required on every social media image

- NMLS #2587985 — Homestead Capital Partners individual

- NMLS #1660690 — NEXA Mortgage, LLC (DBA NEXA Lending) corporate

- Equal Housing Lender wordmark + EHL logo

- "Licensed in 48 states (excluding New York and Massachusetts)" — jurisdiction declaration

- Compliance bar height: ≥20% of canvas (more than DSCR's 18% — HECM disclaimer block adds rows)

📝 Required HECM disclaimer band (in image OR caption)

Borrowers must be 62 years of age or older. HUD-approved counseling is required. A reverse mortgage is not a government benefit. The loan becomes due and payable when the last surviving borrower no longer occupies the home as their primary residence or fails to meet the obligations of the mortgage.

📚 Statutory basis

- SAFE Act: 12 USC § 5103(3); Reg H 12 CFR § 1008.103(e)(7)

- Fair Housing Act: 42 USC § 3604(c); 24 CFR Part 109

- Reg Z: 15 USC § 1601; 12 CFR § 1026.24 + § 1026.33 (reverse-mortgage-specific)

- FHA HECM: 24 CFR Part 206 — counseling + age + non-recourse

- FTC Act §5: 15 USC § 45 — deceptive practices (fear / scarcity language)

- Colorado: C.R.S. § 12-10-707; 4 CCR 725-3

📋 PRODUCT-SPECIFIC HEADLINE PATTERNS

Calm / dignified patterns (NOT urgency)

| Pattern | Example | Frame |

|---|---|---|

| Stay-in-place affirmation | Stay In The Home You Love. | Identity / continuity |

| Equity unlock | Tap Your Equity. Keep Your Home. | Action / reassurance |

| Retirement reframe | Retirement Doesn't Mean Selling. | Reframe pain |

| Tool framing (62+) | After 62, Your Equity Becomes A Tool. | Reframe / agency |

| Choice / dignity | Your Home. Your Equity. Your Choice. | Agency / dignity |

| Plan partnership | A Plan That Works As Hard As You Did. | Earned / respect |

⚠️ Anti-patterns (NEVER use on HECM creative)

- ❌ "Don't lose your home" — fear-based, FTC §5 risk

- ❌ "Government won't help you" — political framing, MAP Rule risk

- ❌ "Free money" / "money you've already earned" — deceptive framing

- ❌ "Hurry / limited time / now" — urgency on senior audience = FTC red flag

- ❌ "Beat your kids out of your equity" — disrespect / family-conflict framing

🎨 Composition principles (HECM senior-audience tuned)

Same neuro/visual research base as AXIA + DSCR, retuned for the 62+ HECM audience. Senior audiences over-index on trust signals; under-index on urgency / scarcity. The whole composition signals "your dignity is intact."

📐 Typography sizing

- Headline cap height: 8–12% of canvas (slightly larger than DSCR; senior readability)

- Subhead: 50–60% of headline pt size

- Compliance footer: 2.5–3% of canvas (legible on mobile)

- HECM disclaimer band: 5–7% of canvas (above compliance bar OR in caption)

- Headline word count: ≤6 words (shorter than DSCR — senior cognitive load)

🎯 Hierarchy patterns (senior-specific)

- Z-pattern for square/portrait — dignified left-right reading

- F-pattern for landscape banners

- Compliance + HECM band bottom anchor — disclaimer reads better as a bottom band, not floating

- High contrast required — older eyes prefer 7:1 contrast minimum (WCAG AAA), not 4.5:1 AA

🟢 CTA color (mortgage-trust signaling)

- Forest green #1F3A2E — HCP brand primary; trust signal

- Gold #C8A96A — premium / earned / dignified — over-indexes with 62+ audience

- Avoid orange / red — urgency colors; both undercut HECM trust framing

- Avoid bright blue — reads as "tech" not "established lender"

📷 Senior photo psychology

- The home is the hero — show the property, not the abstract "happy senior"

- Active retirement beats sad/lonely — couples on porches, gardening, walking, NOT "dependent" framing

- 62+ representation — actual 62+ models, not "young-looking 50" stock

- Avoid hospital / cane / wheelchair imagery — frames HECM as last-resort vs strategic

- Avoid "happy with check" stock — trivializes the decision

- Diverse representation — HECM market is rapidly diversifying; reflect it

🧠 HECM neuro-engagement

- Loss aversion is the wrong lever for 62+ — they have lived it. Lead with identity / continuity / dignity.

- Earned-it framing — "you built this equity; here's how to use it" outperforms "claim what's yours"

- Family-positive, not family-conflict — never frame heirs as adversaries

- Concrete > abstract — "stay in your home" beats "preserve your lifestyle"

- Counseling = quality signal — frame HUD counseling as a benefit / safety net, not a hurdle

📱 Platform algorithm (2026, senior-tuned)

- Facebook is the dominant 62+ platform — over-invest on FB Feed Portrait 1080×1350

- YouTube + connected TV over-index for retirement-planning research

- LinkedIn lower-priority for direct senior targeting; higher for fiduciary / advisor lane

- Larger font sizes — senior viewers stop on legible text faster than designy text

HECM Layout System (Headline + Subhead + CTA + MLO Footer + HECM Band)

Drop ANY HECM headline above into ANY of these dimension templates. Compliance bar = ≥20% of canvas (more than DSCR's 18% — accommodates HECM disclaimer band).

Same Set A 8-size template grid as AXIA / DSCR — retuned for HECM with calm headlines + larger compliance band.

- 01 — FB Feed Portrait 1080×1350 (primary HECM channel)

- 02 — IG Square 1080×1080

- 03 — IG Story 1080×1920

- 04 — FB Feed Landscape 1200×630

- 05 — LinkedIn Single 1200×627 (fiduciary / advisor lane)

- 06 — IAB Leaderboard 728×90

- 07 — IAB MedRectangle 300×250

- 08 — IAB HalfPage 300×600

HECM Composition System (Property + Couple + Calm Text + Compliance Band)

8 composition variants tuned for 62+ audience — show the home, the couple, the dignity. Use as the spec when generating photographic ads via Flux 2 Flex / Ideogram.

- T01 Hero Photo Overlay — full-frame home, headline in negative space, MLO + HECM bar at bottom

- T02 Split 50/50 — property left, headline + CTA right (calm hierarchy)

- T03 Top Photo Bottom Text — couple on porch top, copy + cobrand + MLO + HECM bar bottom (cleanest for compliance — DEFAULT)

- T04 Photo Card Overlay — semi-transparent card over home photo

- T05 Pain → Solution Split — RETIRED for HECM (FTC §5 fear-framing risk on senior audience)

- T06 Testimonial — RETIRED (FTC §5 fake-testimonial risk; same as AXIA / DSCR)

- T07 Process 3-Step — Apply / Counseling / Funded (counseling step is a TRUST SIGNAL — keep visible)

- T08 Stat-Heavy — "Equity Available: $X" big numbers, MUST tie to FHA principal-limit-factor source

- T09 Lifestyle Vignette — gardening / family / travel; NEVER medical / dependency framing

All current HECM creative — review before generation

Every approved Reverse Mortgage creative in current rotation. Click any image to open full-size.

SET A — Text-Only Solid (calm/dignified HECM headlines) (4)

W1_RM_TEXT1

Stay In The Home You Love.

Set A · Text-Only Solid

1080x1080 · ch=I · att=16798 · verified=FHA-HECM

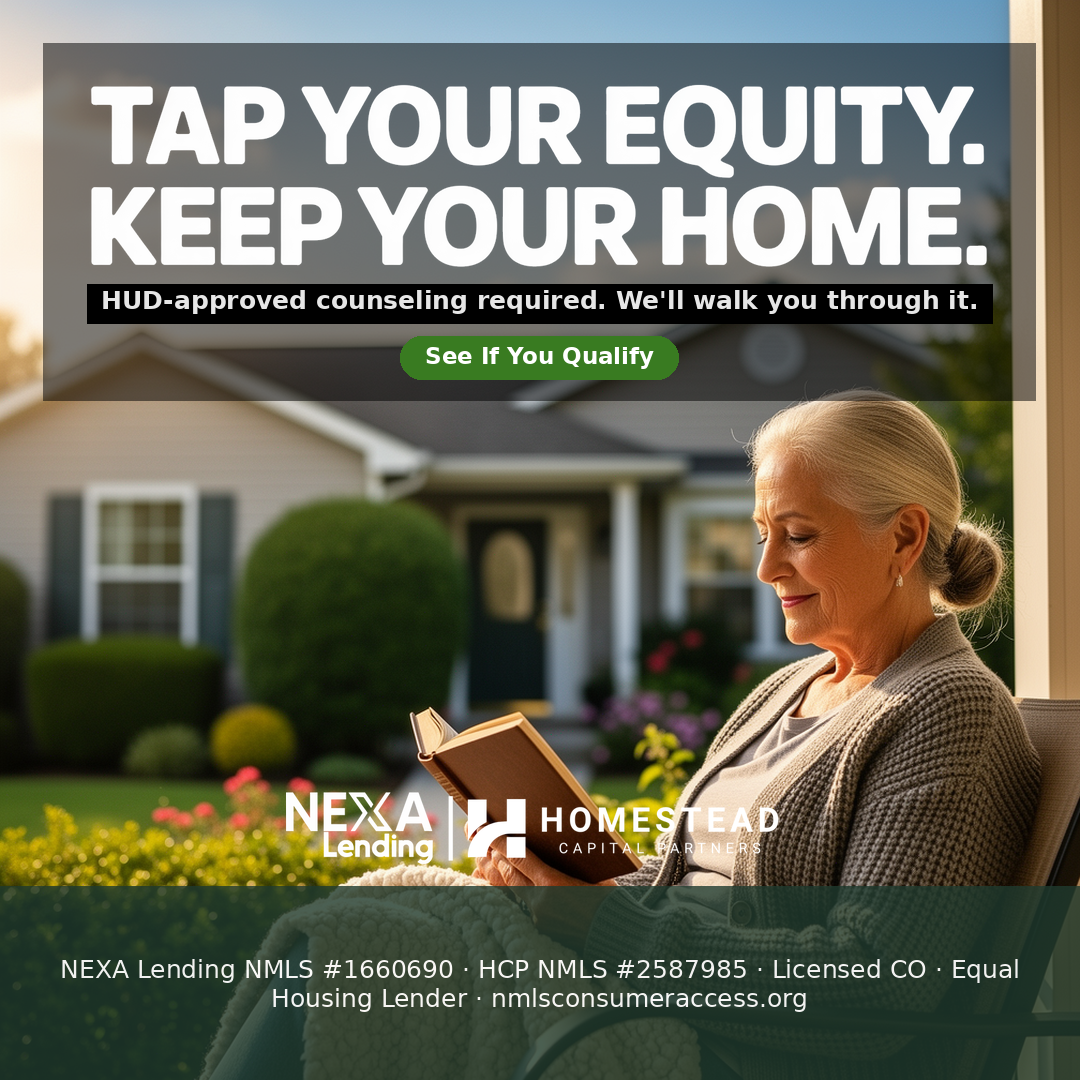

W1_RM_TEXT2

Tap Your Equity. Keep Your Home.

Set A · Text-Only Solid

1080x1350 · ch=F · att=16799 · verified=FHA-HECM

W1_RM_TEXT3

Retirement Doesn't Mean Selling.

Set A · Text-Only Solid

1200x630 · ch=L · att=16800 · verified=FHA-HECM

W1_RM_TEXT4

After 62, Your Equity Becomes A Tool.

Set A · Text-Only Solid

1080x1080 · ch=I · att=16801 · verified=FHA-HECM

SET B · T03 — Top Photo Bottom Text (4)

W1_RM_COUPLE1

Stay In The Home You Love.

Set B · T03 Top Photo / Bottom Text

1080x1350 · ch=F · att=16802 · verified=FHA-HECM

W1_RM_PORCH1

Tap Your Equity. Keep Your Home.

Set B · T03 Top Photo / Bottom Text

1080x1080 · ch=I · att=16803 · verified=FHA-HECM

W1_RM_FAMILY1

A Conversation Worth Having At Sunday Dinner.

Set B · T03 Top Photo / Bottom Text

1080x1350 · ch=F · att=16805 · verified=FHA-HECM

W1_RM_REFI1

Pay Off Your Mortgage. Stay In Your Home.

Set B · T03 Top Photo / Bottom Text

1200x630 · ch=L · att=16807 · verified=FHA-HECM

SET B · T04 — Photo Card Overlay (1)

W1_RM_HANDS1

The Equity You Earned, At 62+.

Set B · T04 Photo Card Overlay

1080x1080 · ch=I · att=16806 · verified=FHA-HECM

SET B · T08 — Stat-Heavy (HECM specifics) (1)

W1_RM_HOUSE1

Set B · T08 Stat-Heavy

1080x1080 · ch=I · att=16804 · verified=FHA-HECM

🔍 Q&A Gates 1–15 + HECM-specific overlays

Every HECM creative ship-decision runs through these 15 gates plus HECM compliance overlay before it reaches Paul.

- Gate 1 — Real logos (no PIL-faked NEXA/HCP/EHL)

- Gate 2 — Ideogram for hero typography (no PIL fonts on headlines)

- Gate 3 — Compliance footer present (NMLS #2587985 + #1660690 + EHL + Licensed in 48 states (excluding New York and Massachusetts))

- Gate 4 — No Reg Z trigger terms without disclosure (rate / payment / down% / term)

- Gate 5 — Cobrand canonical (uses ir.attachment 16767 white-on-dark)

- Gate 6 — Brand standard (NEXA all-caps, HCP wordmark correct)

- Gate 7 — Audience match (62+ senior; calm / dignified, never urgency / scarcity)

- Gate 8 — Focal-point-aware text placement (text in negative space, never on faces)

- Gate 9 — Numerical claims tied to verified FHA source (principal-limit factors / age tables)

- Gate 10 — CTA button spec (≥44pt touch target, ≥7:1 contrast for senior viewers)

- Gate 11 — Headline pattern is calm/dignified (not urgency / not fear)

- Gate 12 — Compliance bar ≥20% of canvas (HECM-specific bigger than DSCR's 18%)

- Gate 13 — Cobrand visibility treatment (~70% block / ~30% drop-shadow rotation)

- Gate 14 — Per-channel dimension correct (FB 1080×1350 = primary)

- Gate 15 — Independent reviewer agent ran (not the generator agent)

🚨 HECM-specific compliance overlays (REQUIRED)

- FTC §5 — no fear / scarcity / "lose your home" framing

- 24 CFR 206 (FHA HECM) — counseling required, age 62+, non-recourse — caption MUST include

- HUD MAP Rule — no "government program" / "free money" framing

- HECM disclaimer band — visible without "see more" expand

🔒 Locked HECM Claims (verification status)

| Claim | Source | Status |

|---|---|---|

| Borrower must be 62+ | FHA HECM 24 CFR 206 | VERIFIED — federal regulation |

| HUD-approved counseling required | HUD HECM rule | VERIFIED — federal regulation |

| Reverse mortgage is not a government benefit | FHA / HUD disclosure | VERIFIED — required disclaimer |

| Loan due when last borrower no longer occupies as primary residence | FHA HECM | VERIFIED — federal regulation |

| Non-recourse loan | FHA HECM | VERIFIED — federal regulation |

| Principal limit factors by age | HUD PLF tables | PENDING — verify which PLF table version (current 2026) |

| NMLS #2587985 (HCP) + NMLS #1660690 (NEXA) | NMLS Consumer Access | VERIFIED |

⏳ What's pending Paul approval before more HECM posts ship

- Headline pattern lock — review the 6 calm/dignified patterns on this page; mark which subset is approved-for-production. (Wave 1 used Stay In The Home / Tap Your Equity / Retirement Doesn't Mean Selling / After 62 Becomes A Tool — confirm continued use.)

- Photo decision (couple-on-porch vs lifestyle-active vs home-only) — Wave 1 leans on couple-on-porch (T03). Confirm or rebalance toward lifestyle-active for Wave 2 to broaden audience perception.

- HECM principal-limit-factor source — pick the canonical 2026 PLF source (HUD ML 2024-XX or current FHA HECM Handbook 4235.1) so T08 stat-heavy creatives can quote actual factors instead of placeholder "up to X% of equity" copy.

🏠 Other HCP creative lanes

DSCR / Investment Real Estate creative (separate compliance lane):

View DSCR Creative →Business funding (AXIA Capital, non-mortgage):

View AXIA Capital Creative →HECM review wall

Internal team reviews live HECM creative + submits revisions:

Open /social Review Wall →